Stablecoin Infrastructure Landscape

Luiz Felipe Barbosa · 10 Jan 2026 · 12 min read

When Stripe paid $1.1 billion for Bridge in October 2024,1 it was one of the largest acquisitions in crypto history. But describing it as a “crypto acquisition” mostly misses the point. Stripe was not buying a blockchain company. It was buying the most mature infrastructure available for solving a problem that has made international payments expensive and slow for decades.

Stripe CEO Patrick Collison put it plainly: stablecoins are “room-temperature superconductors for financial services.”2 The metaphor is apt. A superconductor transmits electricity without resistance — the friction is not inherent to electricity but a property of the material conducting it. Cross-border payments fail not because moving money internationally is physically difficult, but because the infrastructure built to do it was designed in the 1970s and has barely changed since. Stablecoins, in Collison’s framing, could remove the resistance without replacing the underlying current.

This essay examines the infrastructure behind that claim: what stablecoins are, how the on-ramp and off-ramp process works in practice, the competitive landscape of platforms building on top of these rails, and what the Bridge acquisition signals for the future of global commerce.

Understanding the Infrastructure

To appreciate what Stripe acquired, it is necessary to understand the vocabulary of the space — not as an abstract glossary, but because each term maps onto a specific structural failure that stablecoin infrastructure was designed to address.

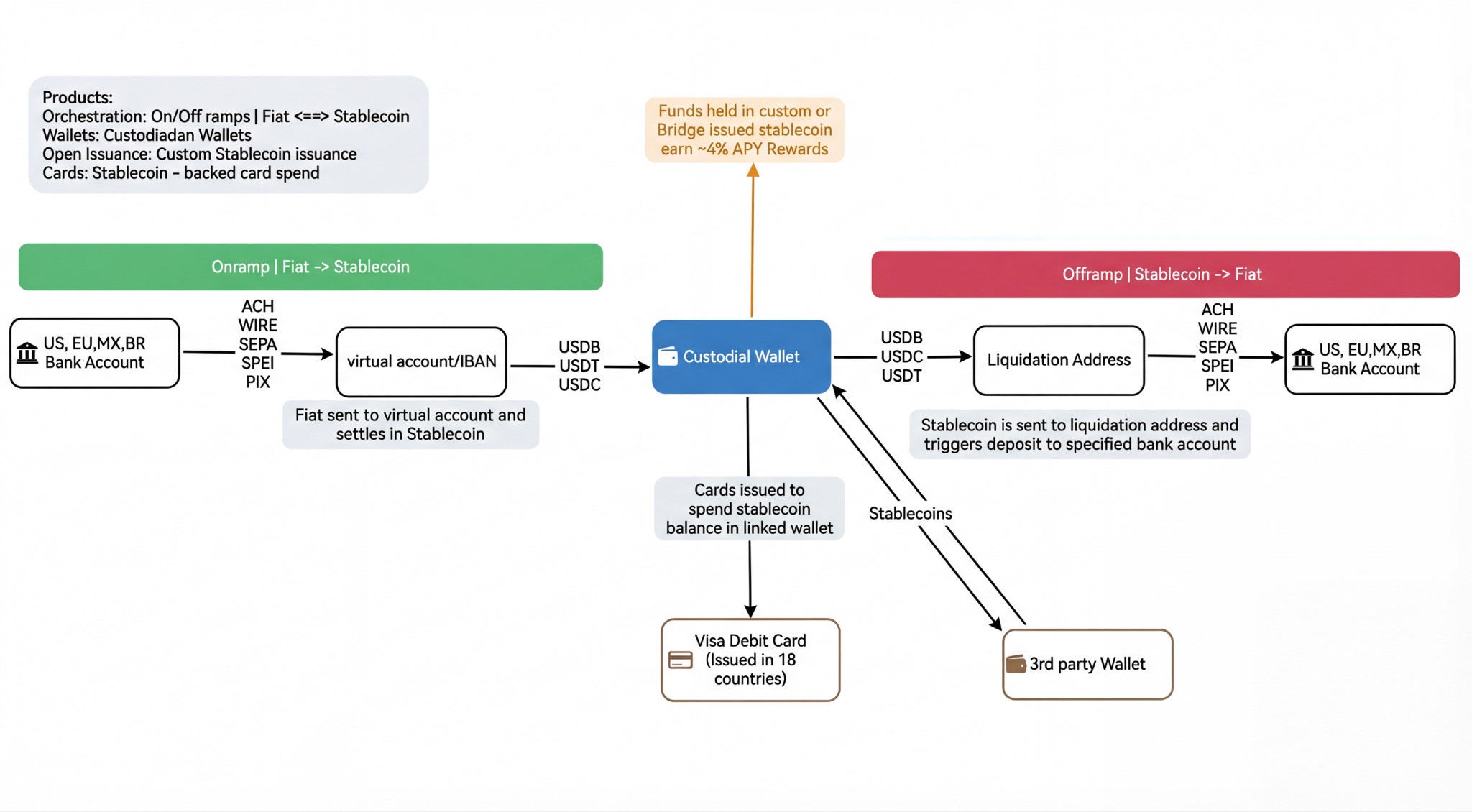

The foundational concept is the stablecoin itself. Unlike Bitcoin or Ethereum, whose prices fluctuate sharply relative to fiat currencies, a stablecoin is a cryptocurrency pegged to a fiat currency — typically the U.S. dollar — through reserve backing. The two most widely used dollar stablecoins are USDC, issued by Circle and backed by fully reserved, audited dollar assets, and USDT (Tether), which draws on a broader reserve composition that has attracted more regulatory scrutiny. Bridge also introduced its own stablecoin, USDB, as part of its issuance product. Regardless of issuer, what these instruments share is that they behave like digital dollars: stable in value, transferable instantly on a blockchain, and settled finitely without a bank as intermediary.3

The terms that matter most for cross-border payments are “on-ramp” and “off-ramp.” An on-ramp is the process of converting fiat currency into stablecoins. A business deposits dollars, euros, reais, or pesos through a conventional payment channel — ACH or WIRE in the United States, SEPA in Europe, PIX in Brazil, SPEI in Mexico — into a virtual account maintained by the infrastructure provider. That deposit triggers the issuance of an equivalent stablecoin amount into a custodial wallet, effectively converting the fiat into digital dollars on-chain. An off-ramp is the mirror operation: stablecoins are sent to a liquidation address, which triggers a fiat deposit into the recipient’s bank account via the appropriate local rail. The speed of that final step — seconds on a real-time rail like PIX or SPEI, a business day on slower systems — determines whether the infrastructure is practically useful in a given market.

A custodial wallet, in this context, is one where the infrastructure provider holds the private cryptographic keys on behalf of the user, much as a bank holds deposits. Most enterprise payment platforms use this model because it integrates more naturally with KYC (Know Your Customer) and AML (Anti-Money Laundering) compliance requirements, which oblige payment platforms to verify customer identities and flag suspicious activity. The alternative — non-custodial wallets, where users hold their own keys — grants more autonomy but places compliance responsibility on the user, making it impractical for most institutional applications.

The bottleneck these stablecoins replace is what the banking industry calls correspondent banking. When a U.S. bank sends money to a counterpart in Nigeria, it does so through a chain of bilateral relationships in which each institution maintains a nostro account — in essence, our money held at your bank — with the next institution in the chain. Every link extracts fees and introduces settlement delay. For major corridors like USD-EUR or USD-GBP, this network functions adequately. For emerging-market corridors — USD-NGN, USD-ARS, USD-BRL at scale — correspondent chains are expensive, slow, and sometimes unavailable. Stablecoin settlement collapses that chain into a single on-chain transaction, handling the foreign exchange conversion once, competitively priced, at the moment of off-ramp delivery.

The Foreign Exchange and Cryptocurrency Markets

The foreign exchange market processes roughly $7.5+ trillion in daily turnover4 — more than any other financial market in the world. It operates with no central exchange, with trades negotiated over-the-counter between banks, institutional dealers, and electronic platforms across the overlapping time zones of London, New York, Tokyo, and Singapore. This decentralized structure functions well for large institutions trading major currency pairs. It functions poorly for smaller transactions, non-major corridors, and businesses in developing economies that must convert local-currency revenue into dollars without absorbing fees of five to eight percent and waiting two to four days for settlement.5

Cryptocurrency presents a structural alternative. Bitcoin, Ethereum, and their peers operate on decentralized blockchains — networks where transactions settle on shared, immutable ledgers without central bank oversight, enabling peer-to-peer value transfer without any participant trusting a single intermediary. The tradeoffs are substantial: exchange insolvency, smart contract vulnerabilities, chain congestion, and regulatory uncertainty introduce risks without clear equivalents in traditional banking. More fundamentally, the price volatility of most crypto assets makes them impractical as payment instruments for businesses that denominate goods and services in dollars.

Stablecoins occupy a distinct position in this landscape. They hold their value in dollars while clearing and settling on a blockchain, which means that a payment from New York to Manila can finalize in seconds for a fraction of a percent, rather than moving through a correspondent banking chain that extracts a toll at every step. The relevant comparison is not FX trading mechanics against crypto trading mechanics but rather correspondent banking against stablecoin settlement as competing architectures for moving value across borders. The former requires bilateral account relationships at every link of the chain; the latter collapses the chain entirely, executing the foreign exchange conversion once, at delivery.

How On-Ramps and Off-Ramps Work

The abstract appeal of stablecoins is straightforward to articulate. The engineering challenge lies in the plumbing: how does a dollar actually enter a stablecoin, traverse a border, and emerge as local fiat currency in a recipient’s bank account? This is the on-ramp and off-ramp problem, and it is where the majority of the infrastructure complexity is concentrated.

In Bridge’s architecture, the flow proceeds as follows. A business or developer initiates a payment through the Bridge API. On the sending side, the customer deposits fiat currency via the appropriate local rail — ACH or WIRE from a U.S. bank account, SEPA from a European account, PIX from a Brazilian account, SPEI from a Mexican account — into a virtual account issued in the sender’s country. Bridge’s system detects the deposit and credits an equivalent amount of stablecoin (USDB, USDC, or USDT) to a custodial wallet. The fiat has been on-ramped.

From the custodial wallet, funds may be held — earning approximately four percent APY on the stablecoin balance — sent to an external wallet, spent via a Bridge-issued Visa debit card available in 18 countries, or directed toward an off-ramp. The off-ramp mirrors the on-ramp in reverse: stablecoins are sent to a liquidation address, which triggers a fiat deposit into the recipient’s local bank account via the designated rail. The stablecoin is redeemed; local currency appears in the recipient’s bank within seconds on real-time systems like PIX, or within a business day on slower infrastructure.

The practical effect of this architecture is that a company paying a contractor in Brazil no longer needs to initiate an international wire, wait for SWIFT settlement, and absorb an FX conversion fee at a correspondent bank. It deposits dollars into a U.S. virtual account, Bridge converts them to USDC on-chain, and the contractor receives reais directly into a local bank account via PIX. The transaction takes seconds. The fee is flat.

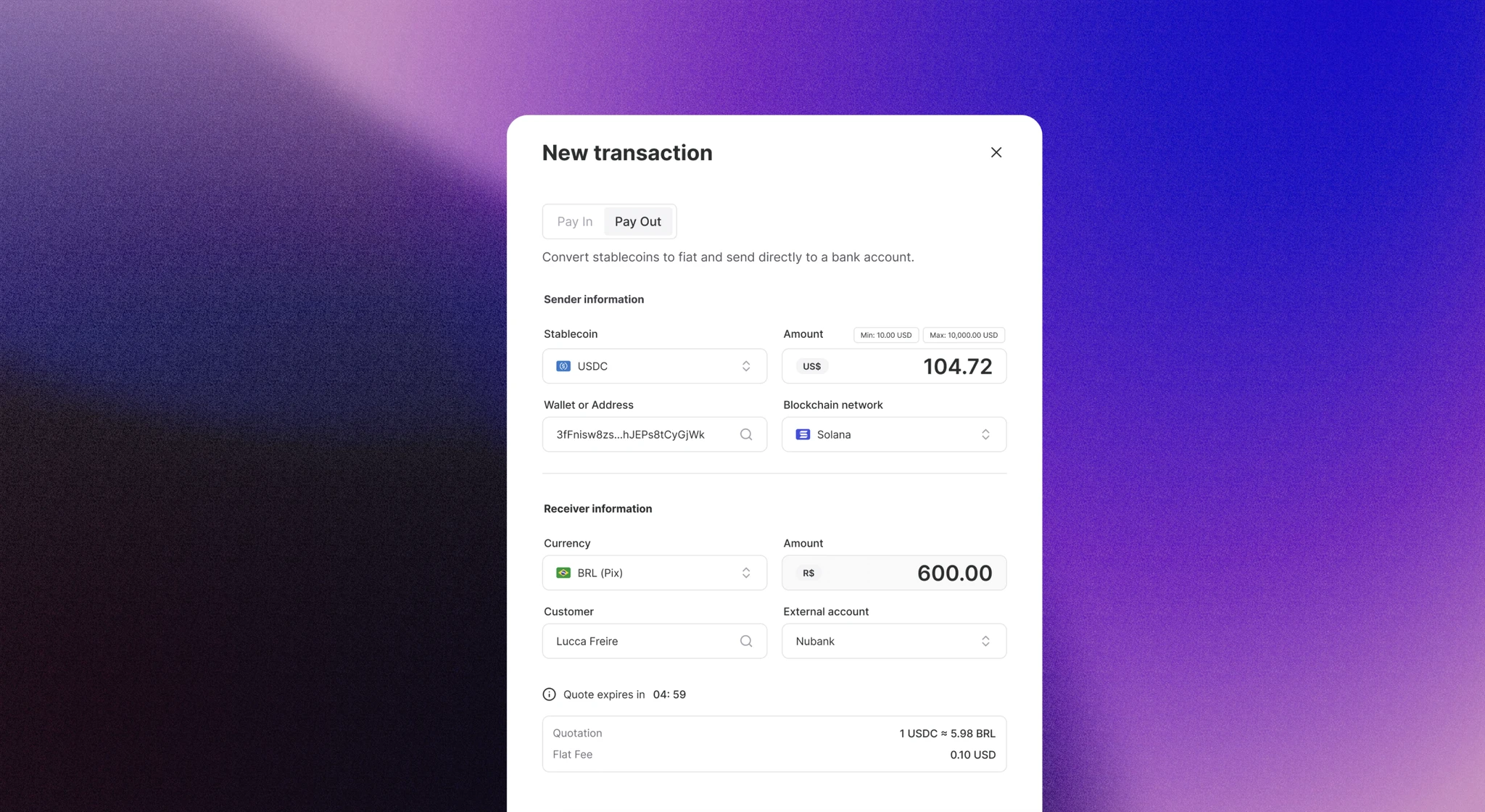

The transaction above illustrates the off-ramp in practice. A sender is converting 104.72 USDC from a Solana wallet into 600.00 Brazilian reais, which will be deposited via PIX directly into the recipient’s Nubank account. The exchange rate is locked at 5.98 BRL per USDC for five minutes, giving the sender certainty while the transaction settles. The flat fee is 15–25 wire fee a traditional bank would charge for the same transfer.

This corridor — U.S. dollars converted to an emerging-market currency and delivered via a real-time local rail — is where stablecoin infrastructure has its most compelling structural advantage. Correspondent banking performs worst in exactly these markets: high FX spreads, limited bilateral relationships, slow settlement. The same calculus applies across dozens of corridors where the legacy system has historically failed: companies in Nigeria receiving USD from U.S. clients, freelancers in Mexico collecting dollar-denominated fees, logistics firms in Southeast Asia managing cross-border payables. Each of these transactions previously required access to a bank with the right correspondent network. With stablecoin infrastructure, they require an API key.

Why Stripe Chose Bridge

Bridge described itself as “Stripe for stablecoins,”6 and the analogy was precise. Stripe had grown into a dominant payment platform by abstracting the complexity of card networks, fraud detection, and processor relationships behind a clean developer API. Bridge pursued the same logic for stablecoin payments: a developer could accept stablecoins, convert between any two dollar formats, and off-ramp to local fiat through a single integration, without managing wallets, gas fees, or blockchain routing directly. The core product comprised three components — orchestration, which handled the movement and routing of stablecoins across chains; issuance, which allowed businesses to mint their own stablecoins backed by treasury reserves with yield shared back to the issuer; and global transfers, which enabled USD-to-local-currency payouts in markets where traditional wire infrastructure was slow or absent.7

The compliance layer was where Bridge most clearly separated itself from its peers. Moving tokens between wallets is a solved engineering problem. Moving tokens in a way that satisfies enterprise KYC and AML requirements, money transmitter regulations, and institutional audit standards is not. Bridge had obtained money transmitter licenses across the United States and was pursuing Electronic Money Institution status in the European Union.8 As Bridge’s Head of Product Mai Leduc put it: “Bridge is compliance-first… we’re not just building tech — we’re engineering trust.”9 In the payments industry, that sentence is operational rather than rhetorical: a license represents years of regulatory work and millions of dollars in compliance infrastructure, and competitors without licenses are structurally limited to crypto-native customers who can accept that risk.

The company’s growth validated the thesis. By 2024, Bridge was processing ten times the volume it had managed the prior year,10 with clients including Coinbase, SpaceX, and several U.S. government agencies. Starlink used Bridge to repatriate peso-denominated Argentine sales revenue — a country where official USD access was severely restricted — converting local receipts into freely transferable stablecoins.11 Nigerian users paid for YouTube Premium subscriptions through Bridge-integrated platforms, using USDC as a workaround for restricted card access. These are not experimental use cases. They are payments that the legacy financial system structurally could not facilitate, and Bridge’s infrastructure was the working solution.

For Stripe, the acquisition addressed a specific gap in its strategic ambitions. Stripe’s stated mission — to “increase the GDP of the internet”12 — presupposes meaningful presence in markets where traditional payment infrastructure is inadequate. Building banking relationships across fifty emerging-market countries takes years and significant regulatory capital. Bridge provided a shortcut. Its issuance capabilities became the foundation of Stripe’s subsequent “Open Issuance” platform, which enables any business to launch its own stablecoin with reserves managed by Stripe and yield returned to the issuer. That product did not exist before the acquisition.

The Stablecoin Platform Landscape

Bridge was not building in a vacuum. By 2024, a range of stablecoin infrastructure platforms had emerged, each targeting specific corridors, customer segments, or use cases. Mapping this landscape clarifies both the scale of the opportunity and the strategic logic of Stripe’s choice of acquisition target.

Yellow Card dominates African payment corridors, operating across more than twenty countries through deep integrations with local mobile money networks and banking systems. Its competitive advantage is geographic specificity — the ability to source liquidity in Nigeria, Ghana, and Kenya in ways that a globally oriented platform cannot easily replicate. That same specificity limits its addressable market.

Due (OpenDue) pursued a different model entirely, offering non-custodial stablecoin accounts that off-ramp to over eighty fiat currencies through local virtual accounts. Rather than building a developer API for other businesses to integrate, Due pursued vertical integration: obtaining local licenses, establishing direct banking relationships in each market, and presenting a consumer-facing product closer in feel to Wise or Revolut than to Bridge.

BVNK provides stablecoin connectivity to financial institutions, linking digital assets to SEPA and Faster Payments rails. Its customers are regulated entities — banks, exchanges, and payment processors — rather than developers or businesses. Unblock Pay focuses on Latin America, enabling stablecoin-to-fiat conversions via PIX in Brazil and SPEI in Mexico; notably, Unblock Pay itself uses Bridge as part of its own infrastructure stack, a fact that signals Bridge’s position as a foundational layer for the category rather than simply one competitor within it. Mural Pay streamlines B2B supply chain payments across the Americas, reducing FX friction in logistics and cross-border procurement. Afriex enables low-cost USDC remittances to Nigeria, Kenya, and Ghana.

The pattern that emerges is consistent: most competitors were regionally focused or built around narrow use cases. Bridge was the only platform with genuinely horizontal ambition — a developer toolkit designed to function in any corridor with any stablecoin. That universality was the specific capability Stripe needed.

Implications for the Payments Industry

Andreessen Horowitz described the acquisition as “the first significant acknowledgment by a mainstream fintech that stablecoins are ready for primetime.”13 That framing may overstate the novelty — PayPal had launched its own stablecoin PYUSD in 2023,14 and Robinhood had acquired a crypto exchange earlier that year — but the Stripe deal was different in institutional weight and strategic intent. A company valued above $100 billion was not adding stablecoin support as a product feature. It was restructuring a portion of its core payment infrastructure around stablecoin settlement.

The transaction volume data helps explain the urgency. In 2024, stablecoins facilitated over $15 trillion in transactions — a figure that rivals Visa’s annual processing volume.15 For any payments infrastructure company, that growth rate raised an unavoidable question: do stablecoins complement traditional card rails, or do they begin displacing them in specific corridors?

The uncomfortable implication of the Stripe-Bridge combination is that stablecoin payments, if widely adopted, would erode card interchange revenue — one of Stripe’s primary income sources. Stripe addressed this tension directly, arguing that new revenue streams — interest on stablecoin float, incremental volume from markets previously outside its reach, and fee-generating services like multi-currency wallets and custom issuance — would more than offset any displacement. The argument assumes stablecoins will scale primarily in corridors where Stripe currently processes little volume, a premise that holds plausibly in the near term and becomes less certain as the technology matures.

Stripe’s 2018 decision to discontinue Bitcoin payments16 after a brief experiment — citing slow settlement, high fees, and insufficient merchant demand — provides a useful point of comparison. The crypto market in 2018 was structurally unfit for commercial payments: volatile pricing, seven-to-ten minute confirmation times, and no regulatory framework. By 2024, USDC offered dollar-stable pricing, sub-second finality on modern Layer 2 networks, and an increasingly coherent regulatory environment. The U.S. Congress passed the GENIUS Act in mid-2025,17 establishing the first comprehensive federal stablecoin framework. Stripe had already closed its Bridge acquisition before that legislation was enacted, meaning it entered the newly regulated environment with a mature and tested product rather than building one in response to the rules.

That timing was not coincidental. Stripe was not reacting to regulatory developments. It was making a calculated bet on where global payment infrastructure would ultimately settle — and acquiring the best-positioned company early enough to help determine the outcome.

Works Cited

- "Stripe Acquires Bridge for $1.1 Billion in Largest-Ever Crypto Acquisition." The Verge, October 20, 2024. theverge.com/2024/10/20/stripe-bridge-acquisition

- Collison, Patrick. "Annual Letter 2024." Stripe, 2024. stripe.com/annual-letter/2024

- Bank for International Settlements. "OTC Foreign Exchange Turnover in April 2022." Triennial Central Bank Survey, September 2022. bis.org/statistics/rpfx22_fx.htm

- World Bank. "Remittance Prices Worldwide." Report No. 47, December 2023. remittanceprices.worldbank.org

- Circle. "USDC: A Dollar Digital Currency." circle.com

- Bridge. "Product Documentation and API Reference." bridge.xyz, 2024.

- Leduc, Mai. "Compliance-First Stablecoin Infrastructure." Bridge company blog, 2024.

- Gaybrick, Will. "Open Issuance: Launching Custom Stablecoins." Stripe product announcement, 2025. stripe.com/blog/open-issuance

- Andreessen Horowitz. "Portfolio Update: Stripe Acquires Bridge." a16z.com, October 2024.

- PayPal. "PayPal Launches U.S. Dollar Stablecoin PYUSD." PayPal Newsroom, August 7, 2023. newsroom.paypal.com

- "Stablecoins Processed More Transaction Volume Than Visa in 2024." Mariblock, January 2025. mariblock.com/stories/stablecoins-grossed-more-transaction-volume-than-visa-in-2024-report

- "Stripe Ends Bitcoin Support." TechCrunch, January 23, 2018. techcrunch.com/2018/01/23/stripe-ends-bitcoin-support

- GENIUS Act (S.394), 119th Congress. U.S. Senate, 2025.

- “J.P. Morgan Wins Big in the $7.5 Trillion FX Market.” J.P. Morgan, www.jpmorgan.com/insights/markets-and-economy/markets/euromoney-fx

More Articles

Middle Out and Bottom Up: The Economic Policy of Joe Biden

1 Dec 2023An examination of Bidenomics—its core tenets of public investment, worker empowerment, and competition—and how the Biden administration’s economic doctrine sought to shift U.S. policy from trickle-down to bottom-up prosperity.

AI Will Replace Designers

15 Jan 2026AI is replacing designers by turning product managers, founders, and engineers into good-enough designers — and once everyone can do the first 80% of the work, the profession gets smaller.

An Analysis of PressTV and Three Privately-Owned Israeli News Channels on Telegram

12 May 2026A comparative NLP analysis of PressTV and three privately owned Israeli Telegram news channels, showing how ownership shapes cadence, topic structure, and media strategy while all four converge around a fear-dominant Iran-Israel-US frame.